🏦 Nexo Review 2026 — Borrow Against Your Bitcoin Instead of Selling It (Credit Line from 2.9%, ZiC 0% APR)

⚡ Quick answer — is Nexo worth it in 2026?

If you hold BTC or ETH through drawdowns and you've ever sold at a loss just to get cash — yes, this product category is built for you, and Nexo is currently the most complete implementation of it. The Credit Line (0.9-12.9% APR in the US) and especially ZiC at an actual 0% APR on BTC/ETH collateral turn your coins into working capital without giving up the upside. The 2026 US comeback on Bakkt's regulated infrastructure makes it a legitimate option for US residents again.

If you live in New York — most of this article doesn't apply to you (ZiC and the Welcome Bonus are both excluded; the regular Credit Line covers most other states). If you borrow at maximum LTV — skip Nexo, skip every lending platform, and reread the risk section below.

🏦 Sign up to Nexo via my referral link

⚠️ Disclosure: this article contains a referral link. If you sign up through it, I may earn a commission at no extra cost to you. One honest caveat the fine print hides: per the official campaign rules, the US Welcome Bonus is not available to accounts registered through referral or affiliate links — if the bonus is your priority, register directly at nexo.com instead. The video review on my channel was made independently and was not paid for by Nexo. Educational content, not financial advice.

🩸 The math most people miss

The market is down, your portfolio is deep in the red, and selling feels like the responsible move. Here's what that decision actually costs.

You bought Bitcoin at $90,000. It trades at $78,000. You sell — and the $12,000 loss stops being a paper loss and becomes a permanent one. Then the uncomfortable part: if BTC bounces back to $90,000 three months later, you missed the entire recovery too. You took the full downside and surrendered the upside.

A crypto-backed loan flips that equation. You keep your Bitcoin, post it as collateral, take cash now — stablecoins or fiat — and repay when liquidity returns. Your coins stay yours through the entire cycle. It's the same playbook corporate treasuries have run for years with every asset class they own; crypto lending just brings it to retail scale. There's also a quieter advantage: in most jurisdictions a loan is not a taxable event, while a sale is.

The price of that flexibility is liquidation risk, and we'll treat it with respect further down.

🏛 What Nexo actually is

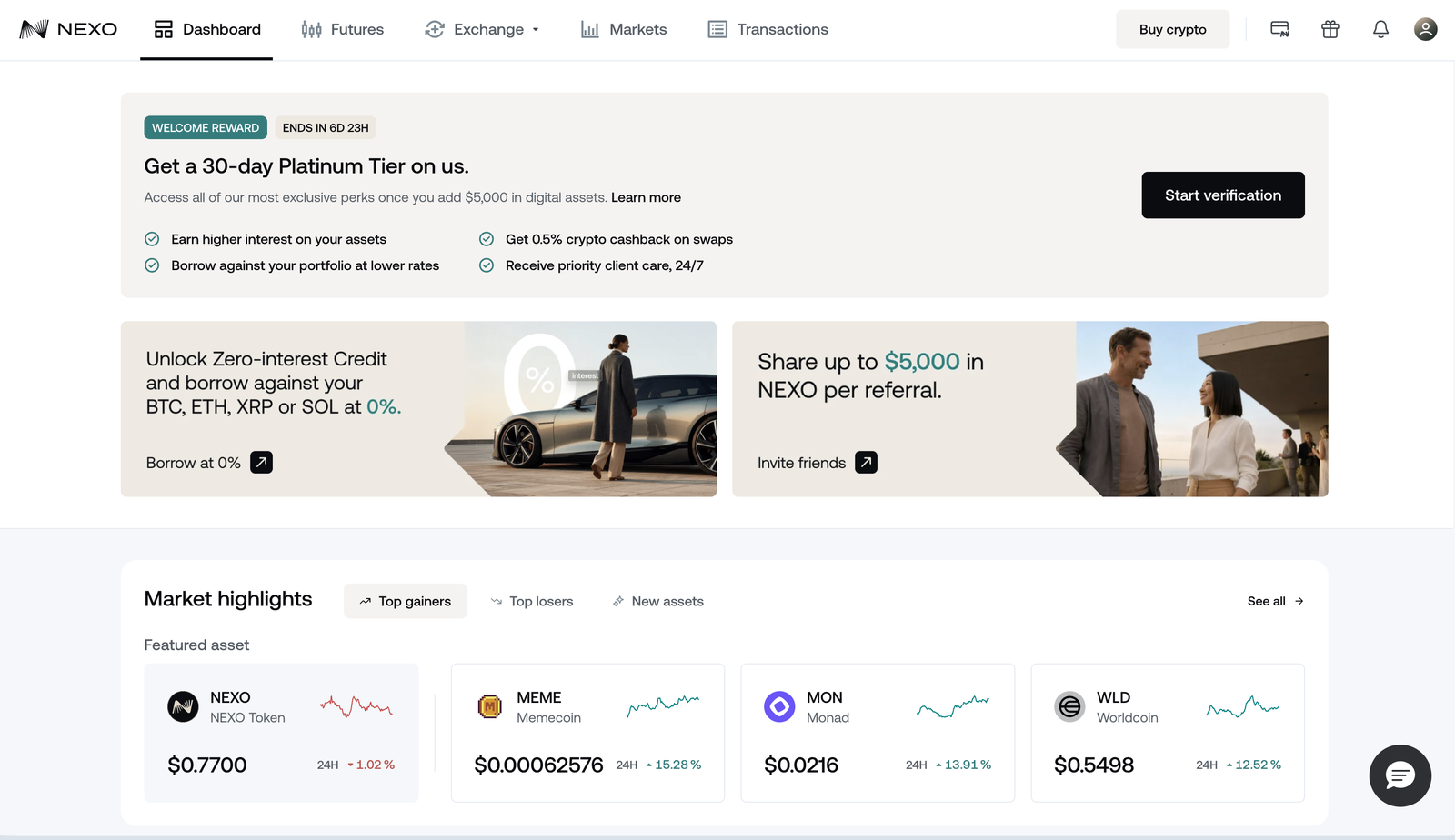

Nexo is not just a lending desk — it's an all-in-one wealth platform for digital assets: earn yield, borrow, and trade from one account. The numbers behind it: operating since 2018, over 7 million users worldwide, $8 billion in assets under management, and $1.3 billion paid out in interest to clients. It's also one of the few CeFi lenders that went through the 2022 Celsius/BlockFi extinction event and came out the other side intact.

The 2026 headline: Nexo re-entered the US market on regulated infrastructure through Bakkt. For US users that's the difference between an offshore product you tolerate and a regulated one you can actually plan around.

🔧 The 8-step walkthrough

This mirrors the full video walkthrough on my channel — screenshots from my own account.

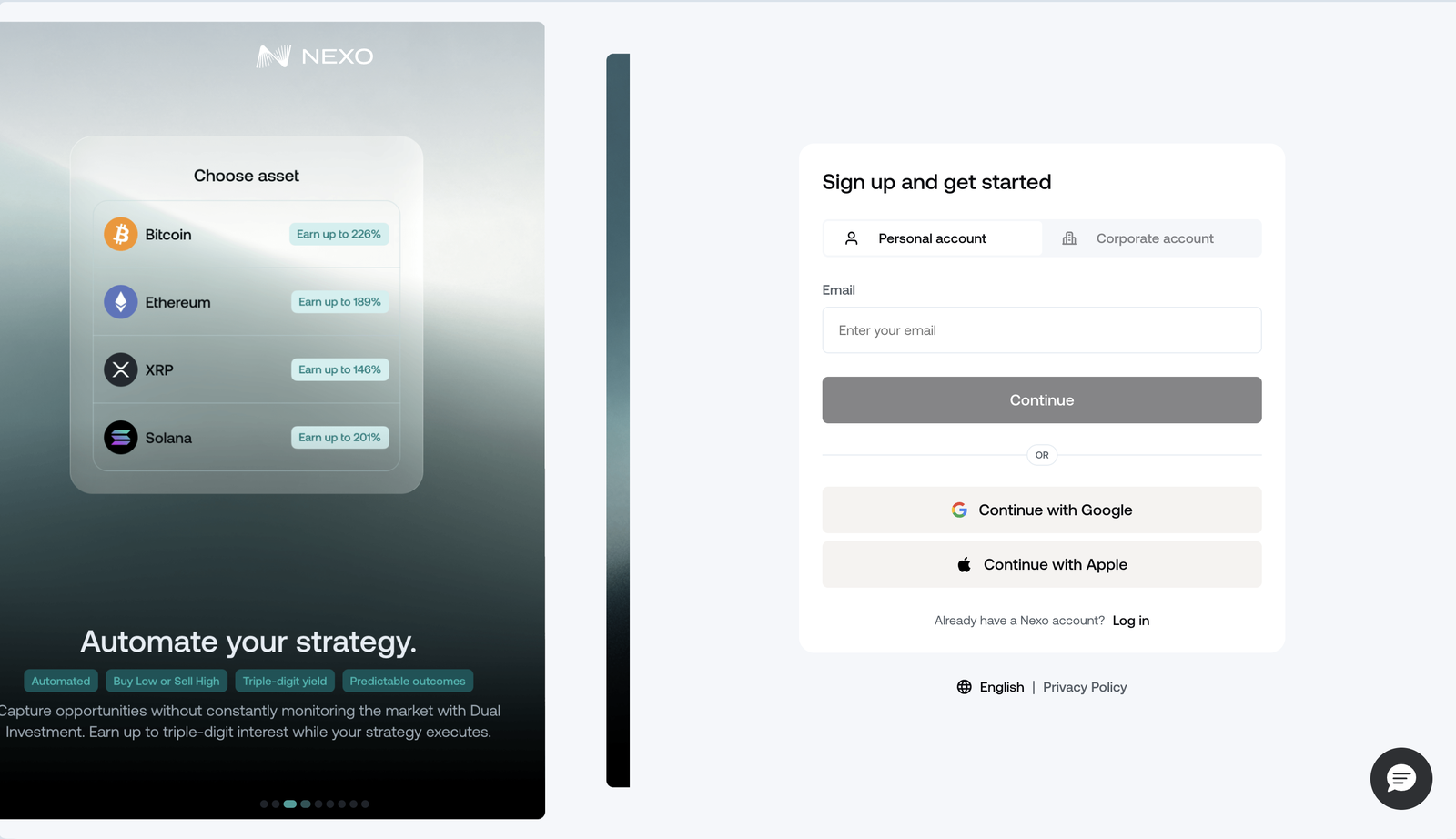

Step 1 — Sign up. Email plus password, or continue with Google/Apple. Takes a minute.

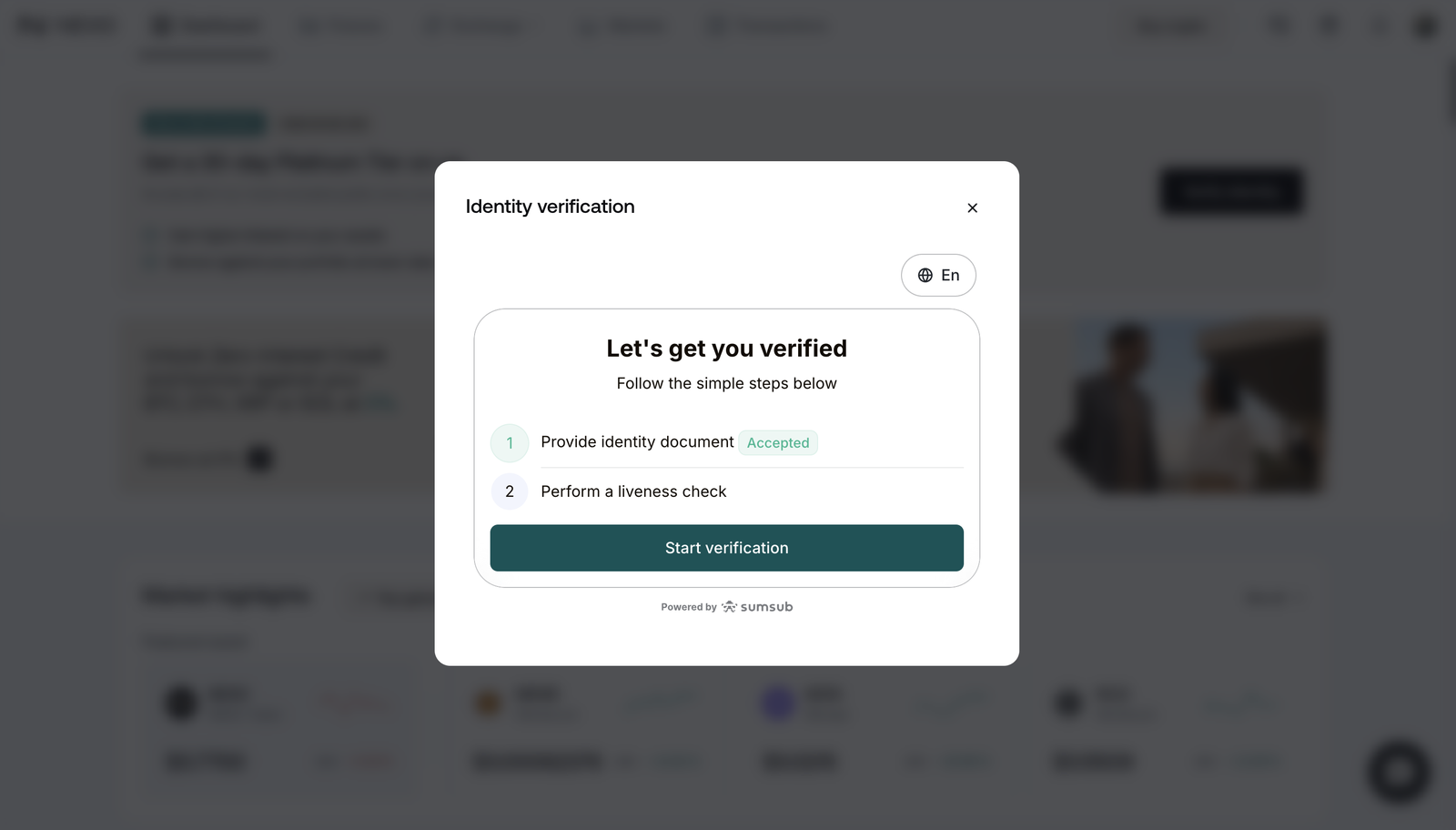

Step 2 — Complete KYC. Standard ID verification: document plus a quick camera check. Mine took under 10 minutes to approve. Full platform access unlocks after this.

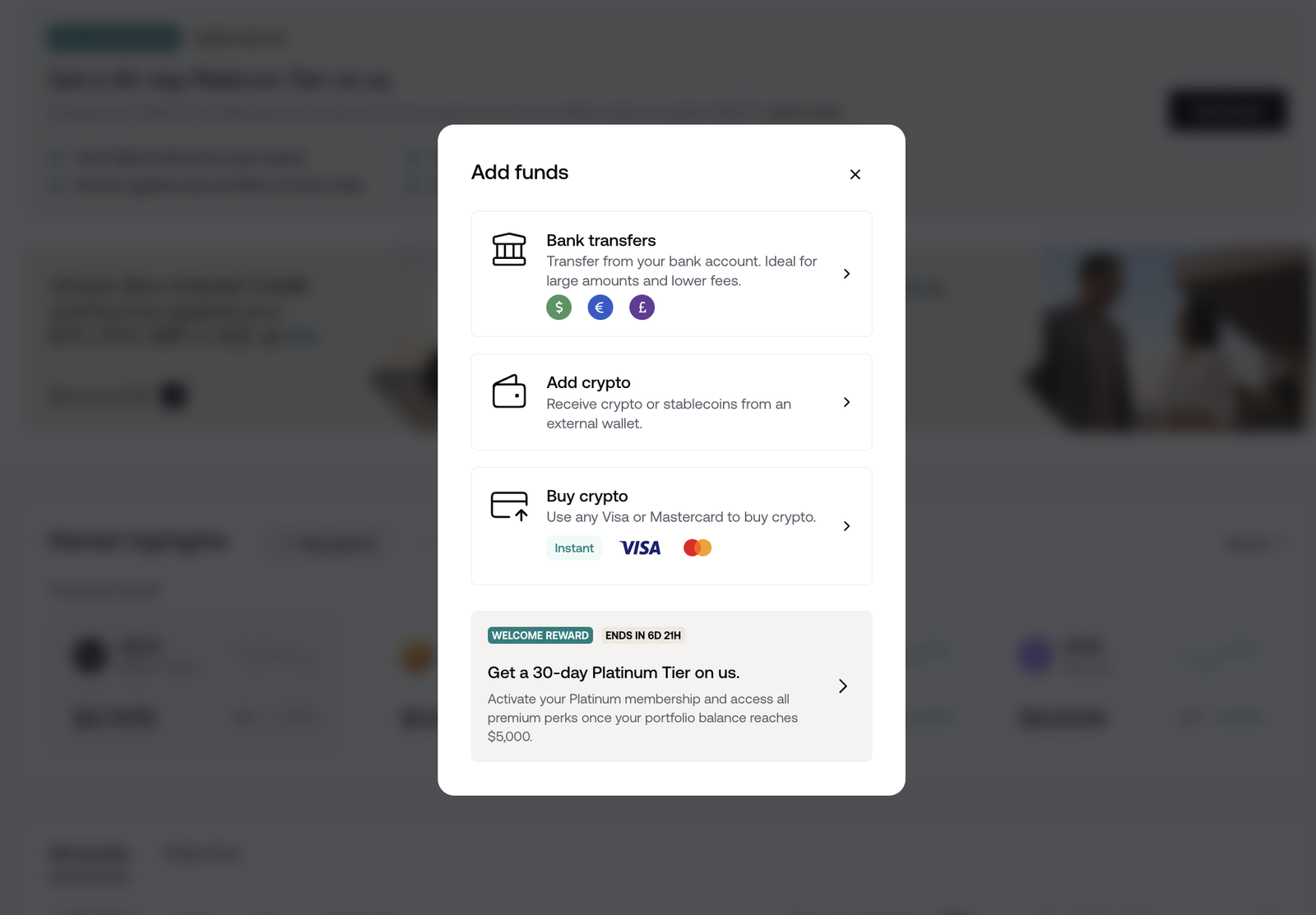

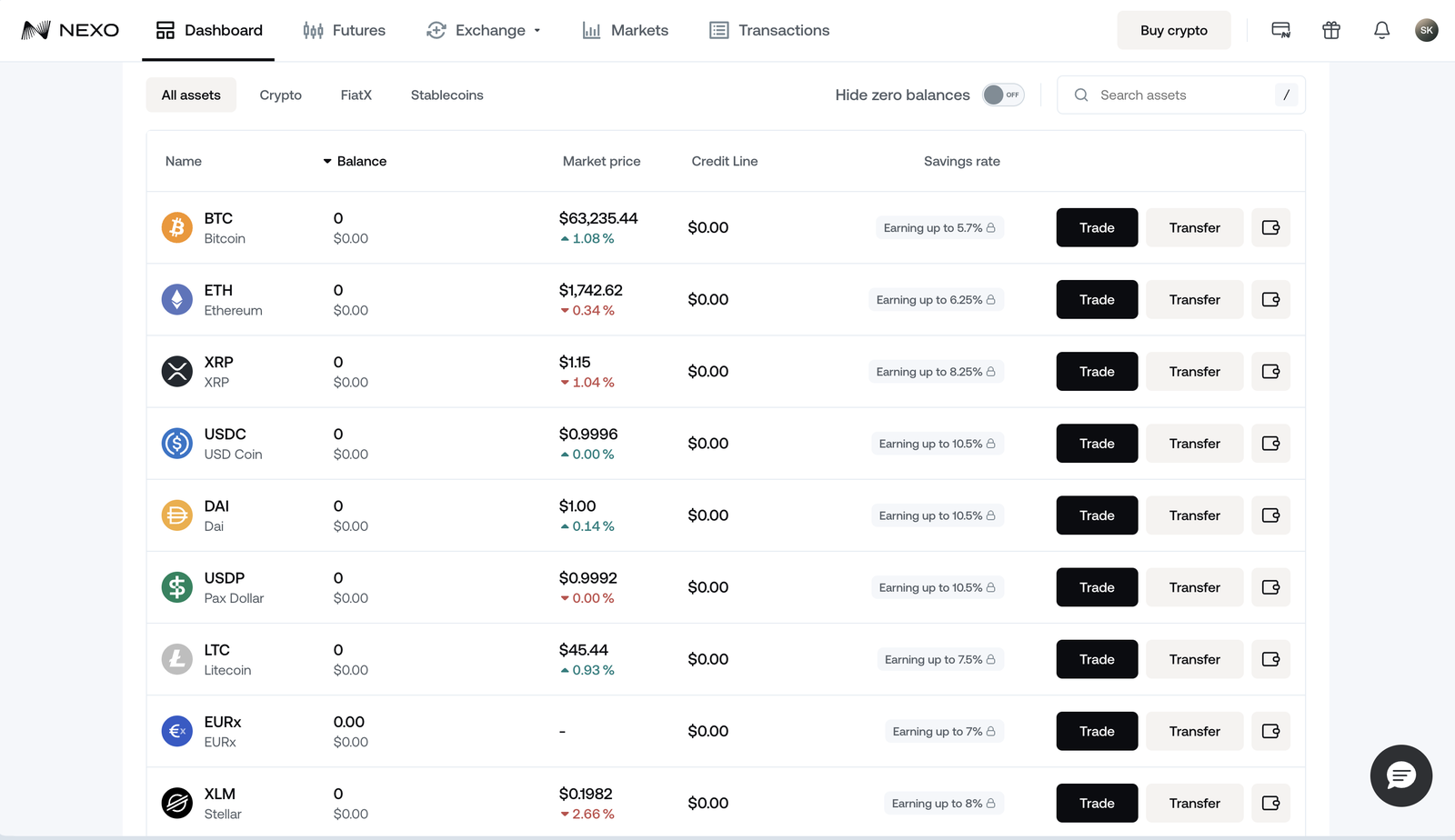

Step 3 — Deposit your collateral. Send BTC or ETH to your Nexo wallet. Pick the right network at deposit and triple-check the address — standard crypto hygiene. The collateral stays yours; it's just now eligible to borrow against.

Step 4 — Open the credit line. Two options here. The regular Credit Line: variable APR depending on loyalty tier and asset, ranging 0.9% to 12.9% in the US. And ZiC — Zero-interest Credit: an actual 0% APR, available for BTC and ETH collateral only.

Step 5 — Choose your loan amount. The platform shows your maximum loan-to-value ratio live. This is the single most important screen in the product: conservative LTV under 30% keeps you well away from liquidation if your collateral drops.

Step 6 — Receive the funds. Stablecoins are instant. Fiat to a bank account typically arrives within 24 hours.

Step 7 — Use the funds. No restrictions: tax bill, car repair, another investment — the borrowed money is yours to deploy.

Step 8 — Repay flexibly. The regular Credit Line repays whenever you have liquidity. ZiC has a fixed term with a predefined repayment range, but extends with one tap before maturity.

💎 ZiC — the headline product

Zero-interest Credit deserves its own section because there's nothing else quite like it on the market right now: actual 0% APR, no fees, no margin calls during the term, and built-in downside protection through Nexo's minimum repayment price mechanism. It won FinTech Breakthrough's 2026 Consumer Lending Product of the Year.

The constraints that make 0% possible: BTC and ETH collateral only, a fixed term with a predefined repayment range (read the range before signing), and the one-tap extension if you need more time. One more constraint: ZiC is not available in New York. The regular Credit Line is available across most US states.

🎁 US Welcome Bonus — what the fine print says

The current campaign gives new US clients 30 days of Wealth Club Premier — Nexo's top loyalty tier:

- Yield: up to 12% annual interest on digital assets

- Credit Line: borrowing rates from 2.9% per year

- Trading cashback: up to 0.5% on trades up to $100,000

To qualify: register, pass KYC, and reach $5,000 in net new deposits within the first 7 days of opening the account. "Net new" means deposits from external wallets or bank accounts; internal transfers from other Nexo users don't count, and withdrawals subtract from the balance.

Now the three lines of fine print that actually matter. New York residents are excluded. Accounts registered via referral or affiliate links are not eligible — yes, that includes mine, so if the bonus is your priority, go directly to nexo.com; if you'd rather support the channel, my referral link is here and I appreciate it. And after 30 days the tier reverts to standard criteria — keeping Premier permanently requires $100,000+ in net assets with at least 10% held in NEXO tokens.

🔒 Security and real talk on risks

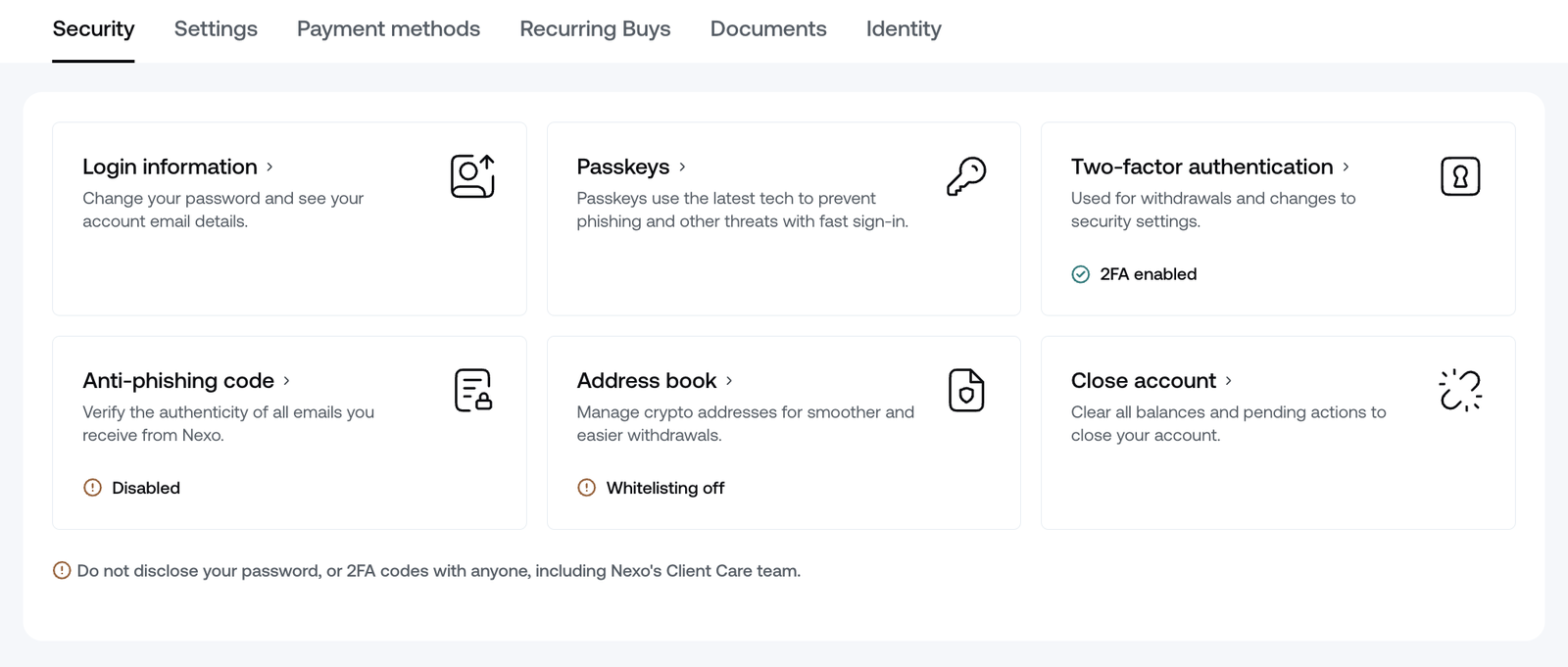

Platform side: Nexo ships the full security stack — 2FA, anti-phishing codes, withdrawal address whitelisting, passkeys. Turn all of it on; it takes five minutes.

Product side — this is the part that separates a useful tool from a margin call at 3am. Crypto-backed loans carry liquidation risk: if your collateral drops far enough below your loan amount, the platform sells it to cover the debt. The mechanics are fair, the timing never is — liquidations cluster exactly when the market is at its ugliest.

The discipline is simple and non-negotiable: keep LTV under 30%, never borrow at the platform maximum, never borrow more than you can comfortably repay from income, and treat the loan as a financial tool, not free money. If you're new to custodial platforms in general, my crypto cards guide covers the same custody logic from the spending side.

🎯 Verdict

For holders sitting on paper losses with real-world liquidity needs, Nexo's Credit Line is the most practical "third option" between panic selling and doing nothing — and ZiC at 0% on BTC/ETH is the best single offer in the lending category right now. The US comeback through Bakkt removes the biggest historical objection for American users. Respect the LTV math, read the bonus fine print before deciding how to register, and the product does what it promises.

▶️ Watch the full 8-step walkthrough on YouTube

🏦 Sign up to Nexo via my referral link

Not financial advice. Always do your own research before depositing crypto on any platform.