2026-02-25 · 2371 words · 12 min

💳 LinkPay Review 2026 — Virtual Visa & Mastercard for Crypto Without KYC, with Facebook Ads / Google Ads / OnlyFans Cards

Full LinkPay review 2026 — non-custodial virtual Visa and Mastercard issued from crypto (BTC, USDT) without KYC verification, Apple Pay and Google Pay integration. Four pricing plans (Lite Free / Plus $59 / Pro $179 / Ultra $209) with progressively lower fees, dedicated cards for Facebook Ads, Google Ads, multi-platform advertising, and OnlyFans withdrawals. Up to 79 free cards per month on Ultra plan, 2% cashback, 50% referral commission. 10 real interface screenshots and honest fee breakdown.

Honest review. Some links are affiliate links: same price for you, a small commission for the project.

⚡ Quick answer — should you sign up?

If you need a virtual Visa or Mastercard issued from crypto without KYC, want to pay for Facebook Ads / Google Ads campaigns reliably, or run an agency with team-card management — yes, LinkPay is structurally unique and worth signing up. Free Lite plan to start, no-KYC virtual cards in seconds, Apple Pay and Google Pay support, dedicated cards for ads platforms that bypass the chronic decline problem of standard cards.

If you just need a basic spending card with cashback and you're already in the Bybit / OKX / Pionex ecosystem — those CEX cards are simpler and better for that specific use case. LinkPay's edge is in no-KYC + agency / ads-buying scenarios, not pure retail spending.

💳 Sign up to LinkPay through my referral link

⚠️ Disclosure: this article contains an affiliate link to LinkPay. If you sign up through it, I may earn a commission at no extra cost to you. LinkPay is responsible for its own product, terms, and security claims — verify everything on linkpay.io before depositing meaningful capital. Educational content, not financial advice.

🩸 Context — the crypto-to-fiat infrastructure gap

The market is shifting right now and if you aren't paying attention to the infrastructure layer, you're missing the entire point of this cycle. We all love seeing portfolios pump, but the biggest pain point in crypto isn't buying the dip — it's actually using your gains in the real world without jumping through a million hoops.

The current state of crypto-to-fiat off-ramps:

- Centralized exchanges tighten the screws with more regional restrictions, KYC requirements, and arbitrary card cancellations

- Old-school crypto cards have insane fees (3-5% transaction + FX) or regional locks

- P2P off-ramps carry counterparty risk and AML scrutiny

- Ad platforms (Facebook / Google / TikTok) routinely decline standard payment methods, making it impossible to scale advertising spend

LinkPay bridges this gap with a focused no-KYC, business-friendly product line.

💳 LinkPay — what it actually is

LinkPay is a non-custodial fintech platform that converts your crypto deposits (BTC, USDT) into virtual Visa or Mastercard balances issued in USD or EUR. The user flow:

- Sign up at linkpay.io with email, Gmail, or Telegram

- Verify email immediately to unlock the full feature suite

- Issue a virtual card from one of four categories

- Send BTC or USDT to the designated deposit address

- Funds auto-convert to USD or EUR and load to your card

- Add the card to Apple Pay or Google Pay

- Spend anywhere Visa or Mastercard is accepted

The crypto deposit conversion happens at the moment of the deposit, not custodied long-term as crypto. This makes LinkPay structurally different from leaving crypto on a CEX waiting to spend.

🎯 Four card categories — for different use cases

LinkPay's card lineup is built around specific spending verticals, not generic "crypto cards":

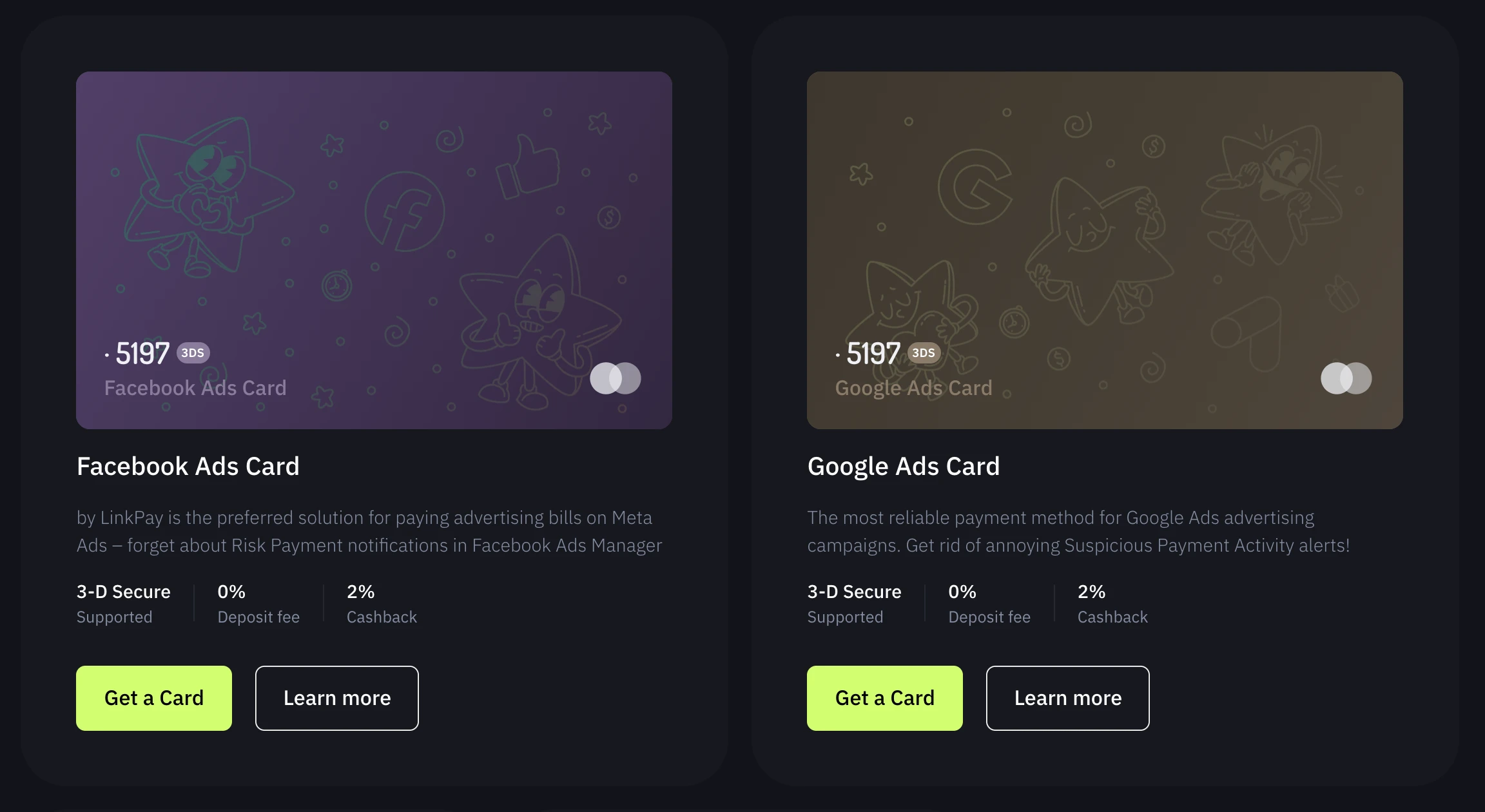

📱 Facebook Ads Card + Google Ads Card

Facebook Ads Card is the preferred solution for paying advertising bills on Meta platforms (Facebook, Instagram). It eliminates the chronic Risk Payment notifications that destroy ad accounts when you use standard cards. If you've ever had Facebook freeze your billing or randomly flag a payment method, you know how critical this is.

Google Ads Card does the same for Google Ads — eliminates "Suspicious Payment Activity" alerts and reduces account suspension risk.

Both cards: 3-D Secure supported, 0% deposit fee, 2% cashback on Ultra plan.

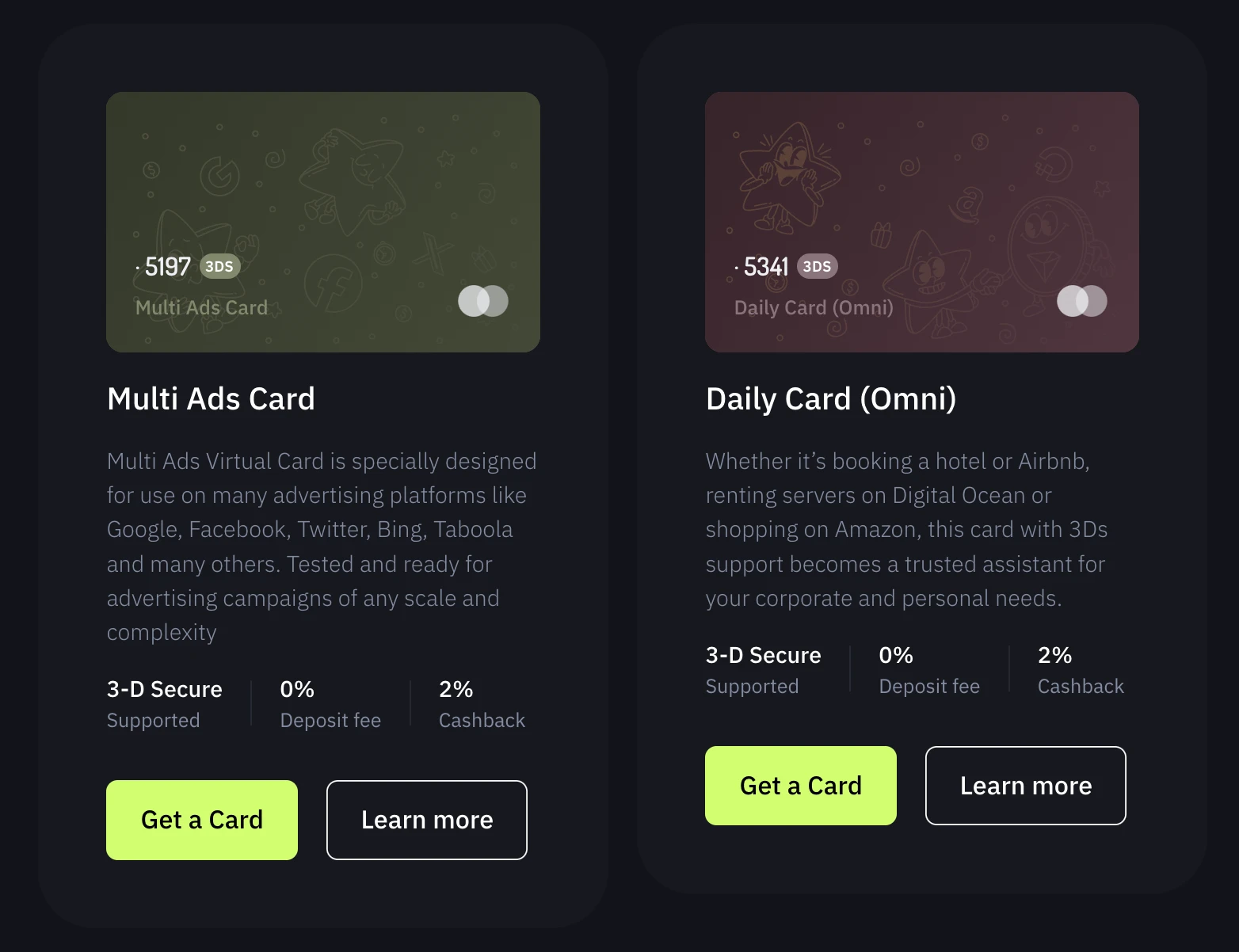

🌐 Multi Ads Card + Daily Card (Omni)

Multi Ads Card is specially designed for advertising platforms beyond Meta/Google — works on Twitter, Bing, Taboola, and many others. Tested and ready for advertising campaigns of any scale and complexity.

Daily Card (Omni) is the universal card for everyday purposes: booking hotels or Airbnb, renting servers on Digital Ocean for hosting, shopping on Amazon, and any other web purchase. The "Omni" naming reflects its omnivorous compatibility — this is what you use when you don't need an ads-specialized card.

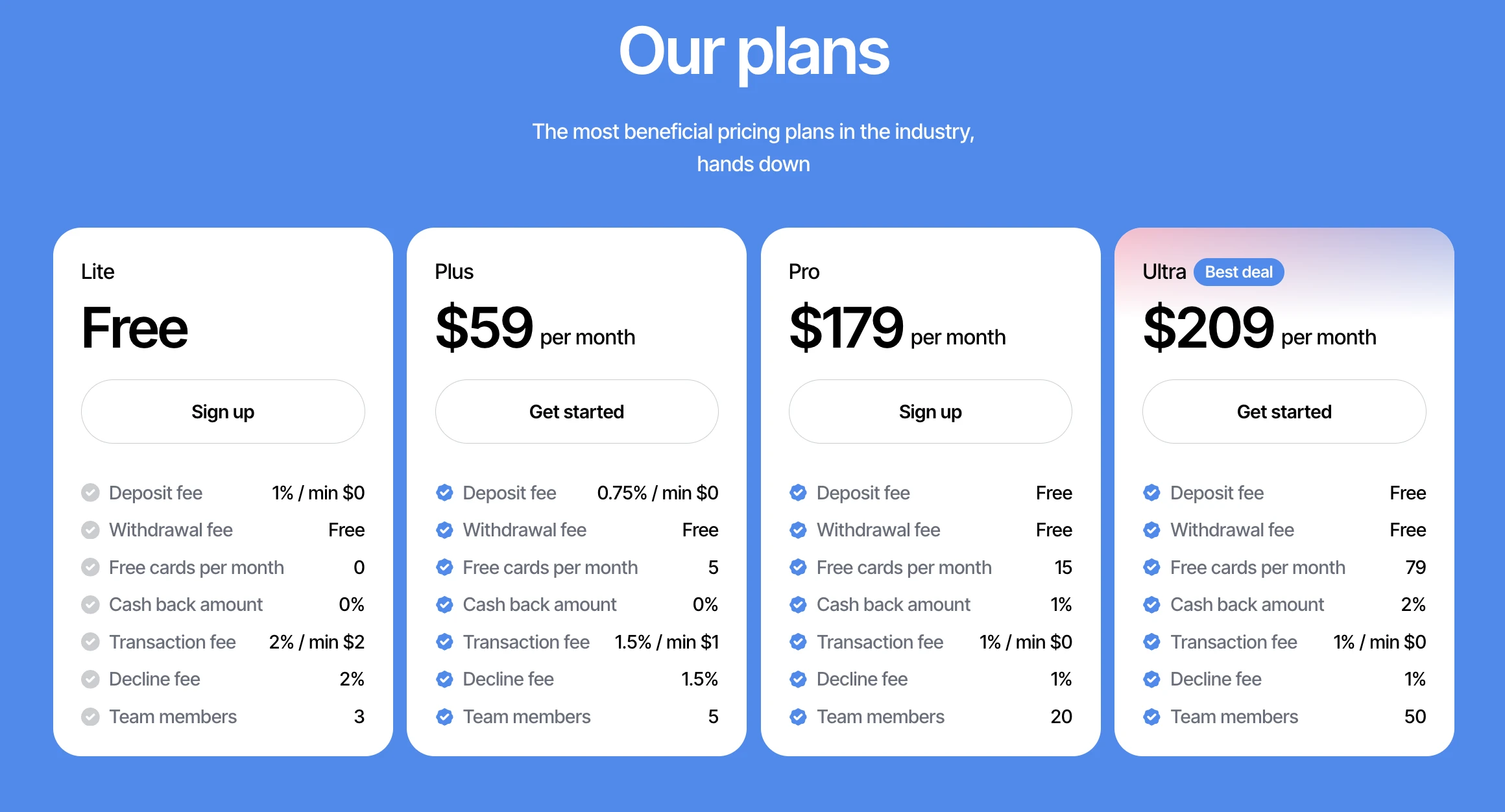

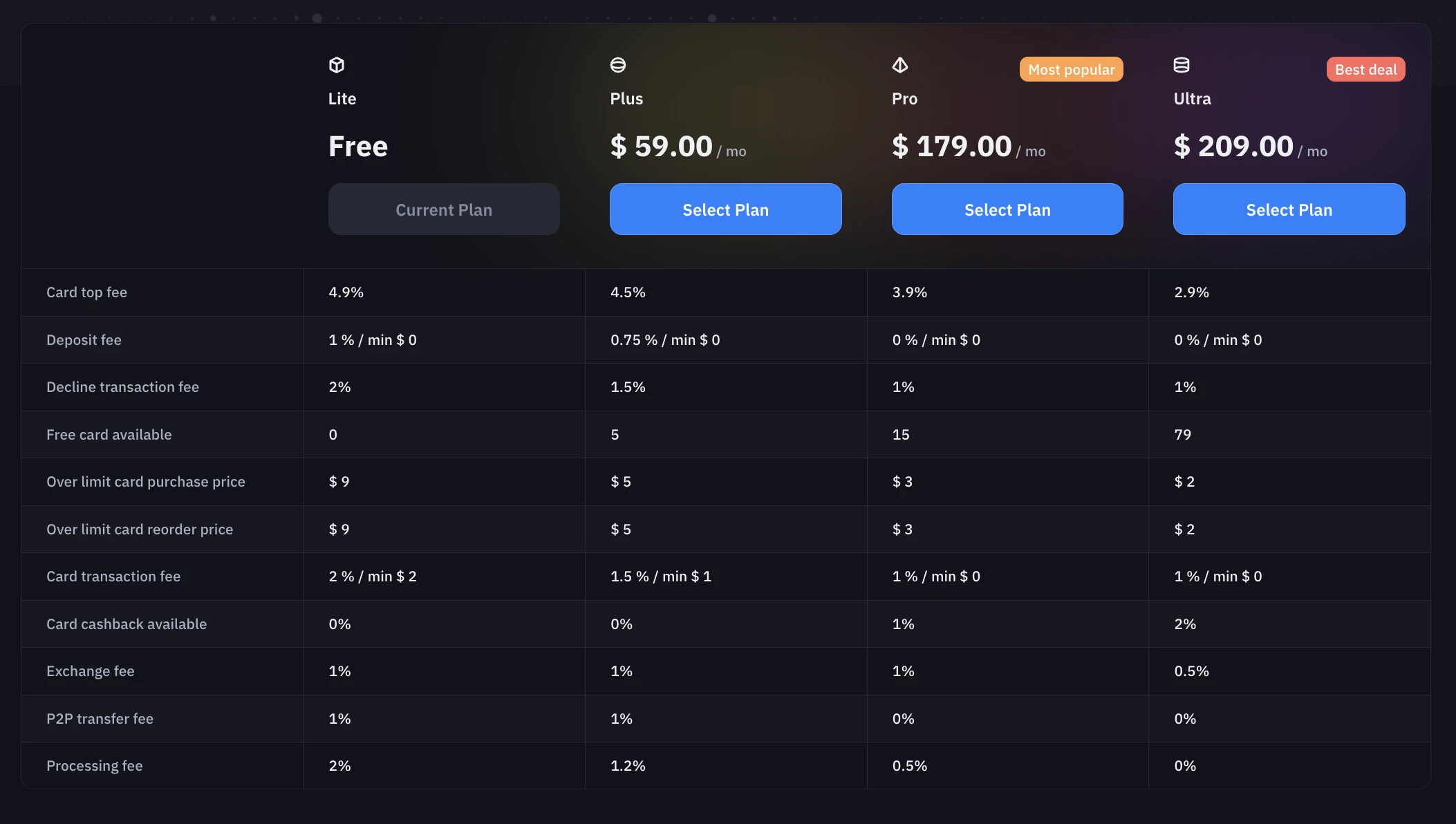

💰 Pricing — four plans honestly compared

Four plans with progressive fee reductions:

| Parameter | Lite (Free) | Plus ($59) | Pro ($179) | Ultra ($209) |

|---|---|---|---|---|

| Deposit fee | 1% / min $0 | 0.75% / min $0 | Free | Free |

| Withdrawal fee | Free | Free | Free | Free |

| Free cards per month | 0 | 5 | 15 | 79 |

| Cashback | 0% | 0% | 1% | 2% |

| Transaction fee | 2% / min $2 | 1.5% / min $1 | 1% / min $0 | 1% / min $0 |

| Decline fee | 2% | 1.5% | 1% | 1% |

| Team members | 3 | 5 | 20 | 50 |

Detailed comparison with all fee categories:

The full picture includes additional fees:

| Parameter | Lite | Plus | Pro | Ultra |

|---|---|---|---|---|

| Card top fee | 4.9% | 4.5% | 3.9% | 2.9% |

| Cash back available | 0% | 0% | 1% | 2% |

| Exchange fee | 1% | 1% | 1% | 0.5% |

| P2P transfer fee | 1% | 1% | 0.5% | 0% |

| Processing fee | 2% | 1.2% | 0.5% | 0% |

Break-even math:

- Lite (Free) — pays nothing upfront, but 4.9% card top + 2% transaction means $1,000 of spend costs ~$70 in fees. Use only for occasional small purchases.

- Plus ($59/mo) — break-even from ~$1,300/month of card spending (saves enough on lower transaction fees vs Lite)

- Pro ($179/mo) — break-even from ~$5,000/month, plus 1% cashback offsets the monthly fee at ~$18K spending

- Ultra ($209/mo) — break-even from ~$11,000/month spending (2% cashback alone = $220 on $11K), realistically optimal for $15K+ monthly volume

For ad agencies running $10K+ per month per campaign across multiple platforms, Ultra is the obvious choice — 2.9% top + 1% transaction + 2% cashback + 79 free cards + 50 team members tightly fits the use case.

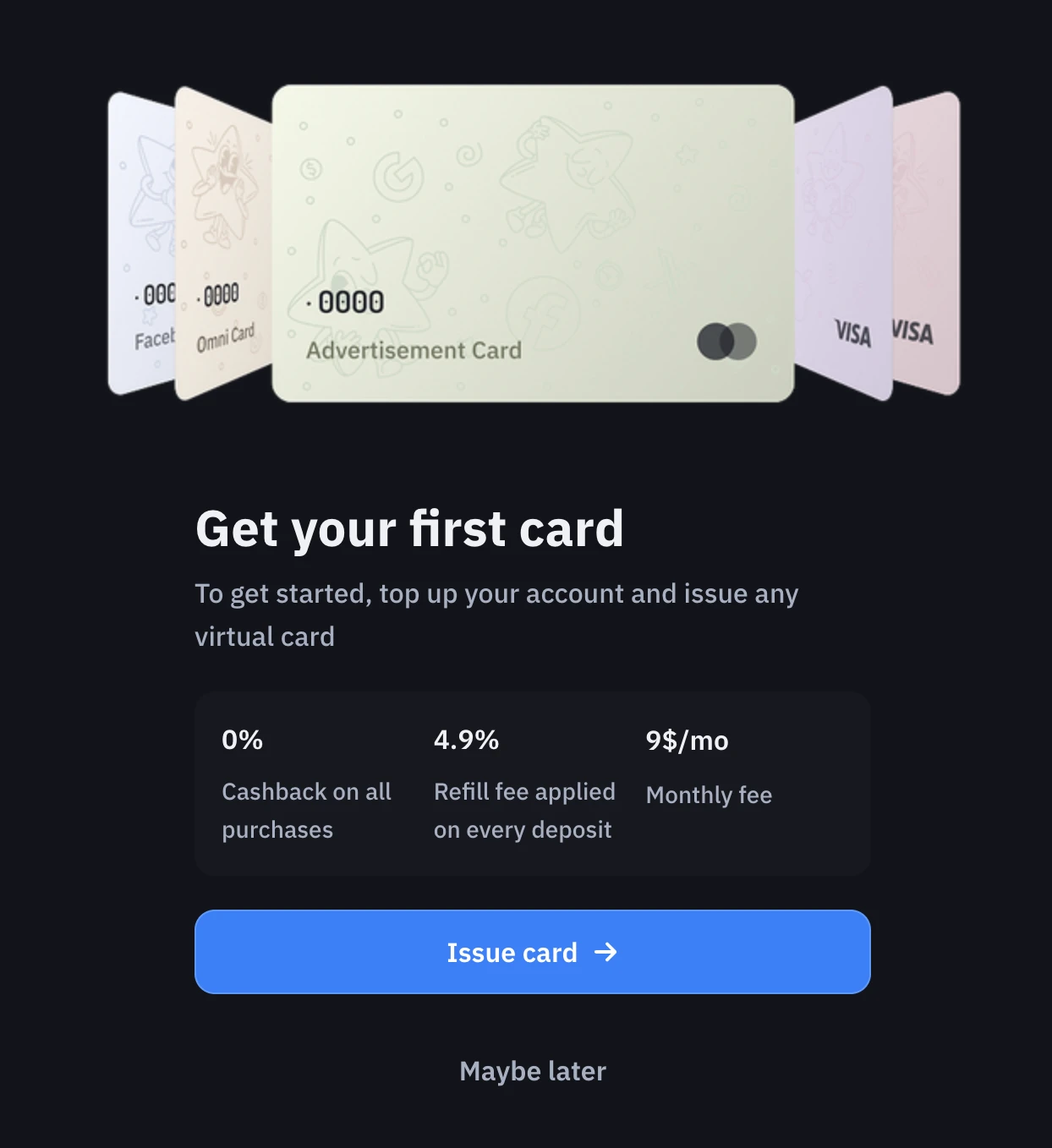

🔧 Getting your first card — the actual flow

LinkPay's onboarding is built for speed. Three-screen flow from dashboard to active card:

Step 1: Issue card dialog

Important honesty check: this is the default card without subscription plan. The terms are:

- 0% cashback on all purchases

- 4.9% refill fee on every deposit (this is the highest tier)

- $9/month monthly fee per card

If you want better economics, subscribe to a plan first (Plus/Pro/Ultra) which brings deposit fee down to 0% and adds free cards / cashback. The default card is fine for testing or one-off purchases but expensive at scale.

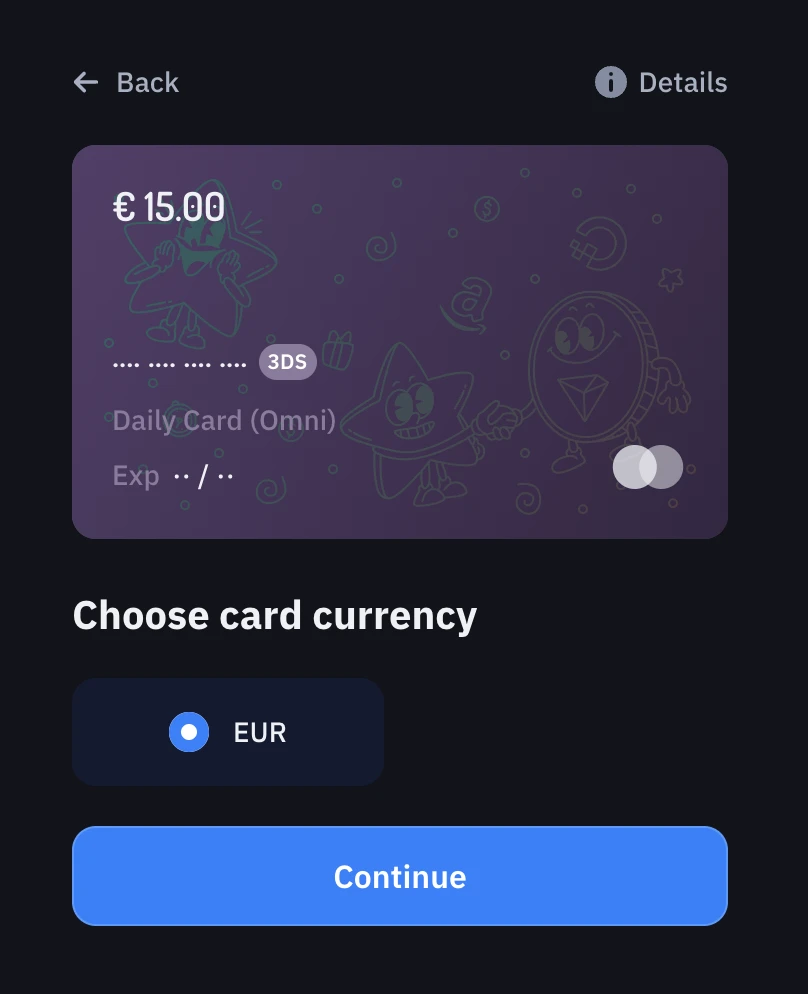

Step 2: Choose currency

USD or EUR are the only options. Pick based on where you spend most:

- EUR if you live in Europe or buy mostly EUR-denominated services

- USD for international ads platforms, US services, most SaaS

You can issue multiple cards in different currencies if needed (subject to your plan's free-cards limit).

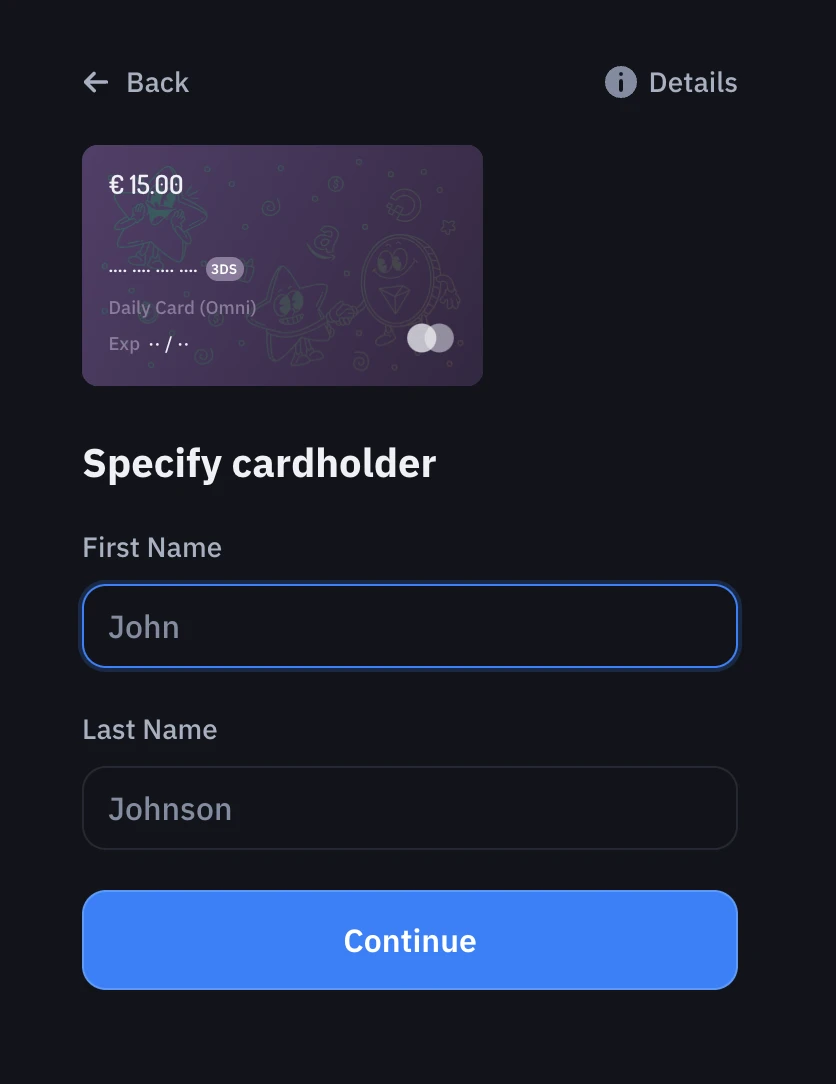

Step 3: Specify cardholder

This is where the no-KYC nature is visible: you literally type First Name and Last Name as text fields. There's no document upload, no liveness check, no address verification. Some merchants may require name-on-card to match billing details during 3-D Secure flow, so use a name you can defend if asked, but no third-party validates the data.

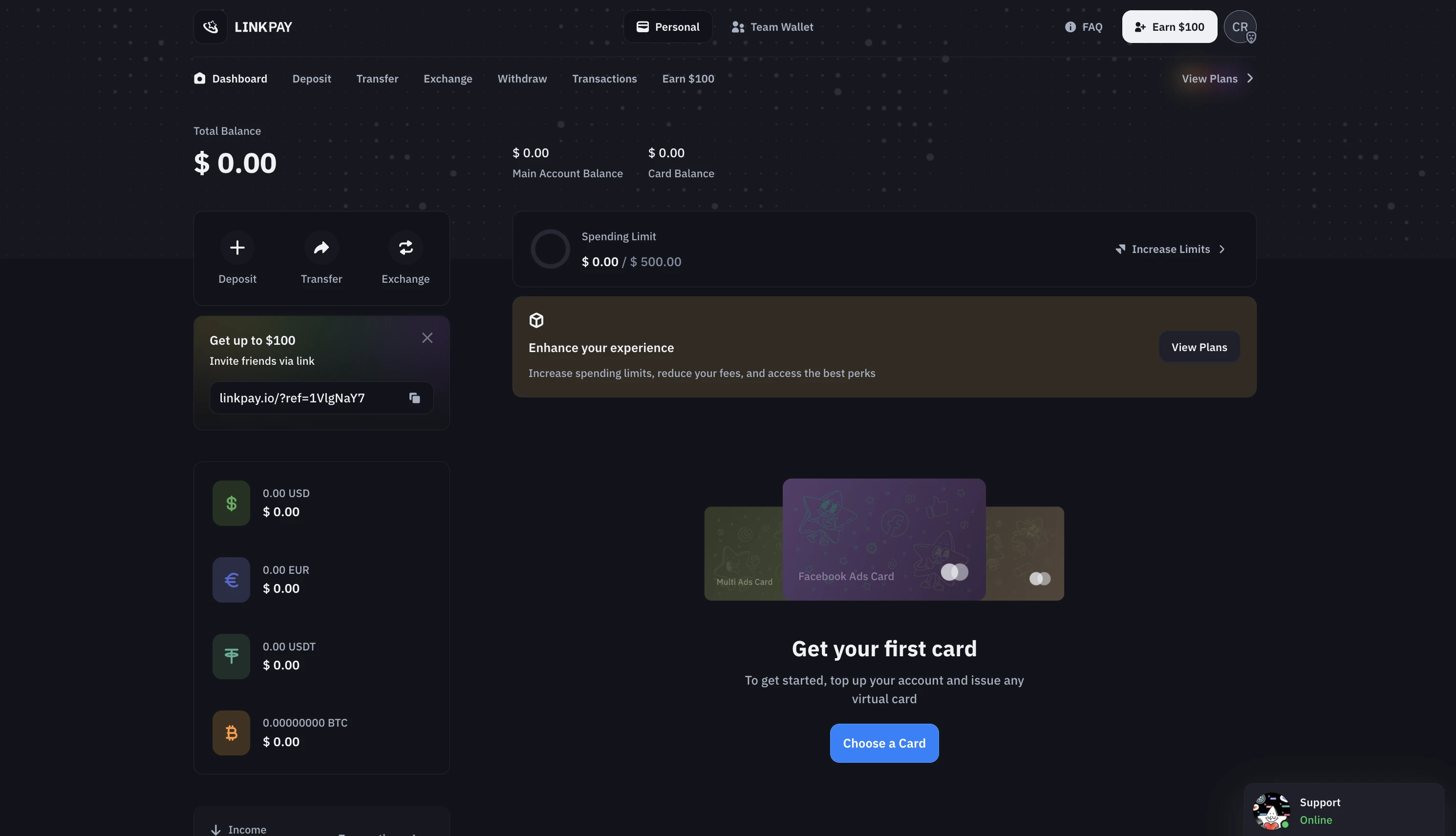

📊 Dashboard — what you actually manage

The dashboard is clean, data-driven, and zero fluff. Main areas:

- Total Balance at the top with USD/EUR/USDT/BTC breakdowns

- Quick actions: Deposit, Transfer, Exchange, Earn $100 referral

- Top nav: Personal / Team Wallet / FAQ

- Action buttons: Dashboard / Deposit / Transfer / Exchange / Withdraw / Transactions / Earn $100

- Get up to $100 promo with one-click referral link copy

- Card management at the bottom with currency-specific balances

- Spending Limit widget showing current usage against your card cap

- Live support widget (web chat) bottom right

The interface stays out of your way — no useless charts, no manipulation prompts. You manage liquidity and issue cards, period.

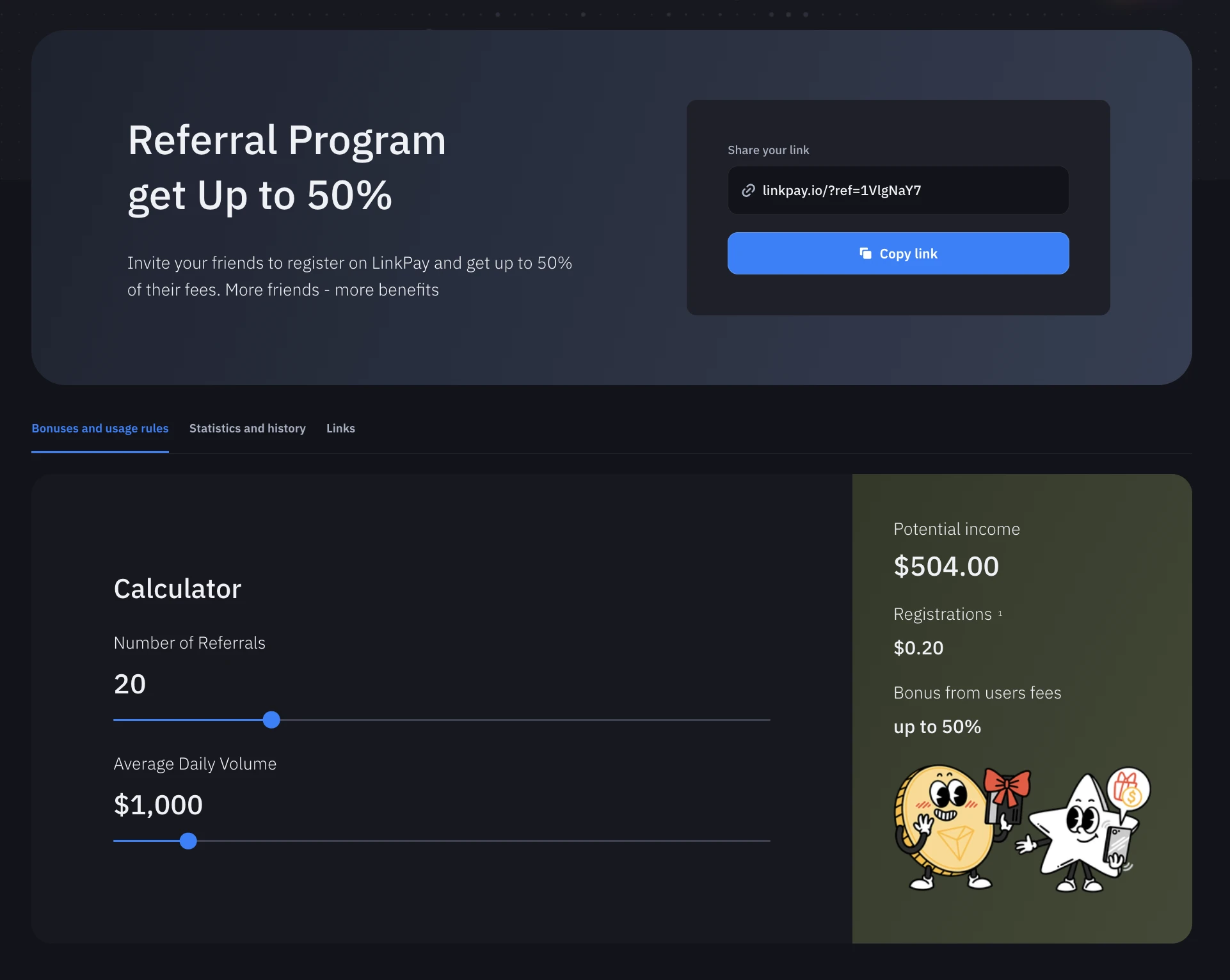

👥 Referral program — up to 50% commission

LinkPay's referral economics:

- Up to 50% commission on all fees paid by users you refer

- $0.20 per registration (small flat fee)

- Real-time tracking in the LinkPay dashboard

Calculator example from the screenshot: 20 referrals each with $1,000 average daily card volume generates ~$504/month potential income. This is more competitive than typical CEX affiliate programs (Bybit's tops out around 30%, Binance around 40%).

The model rewards active users — passive signups contribute minimally, but referrals who actually use cards at meaningful volume generate ongoing income.

💼 For businesses, agencies, and media buyers

LinkPay's strongest vertical is the agency/ads-buying use case. Key features:

- Team cards — issue cards for staff members from one master dashboard

- Granular spending limits per card (per-card monthly caps, transaction limits, category restrictions)

- Centralized tracking — see every transaction across all team cards in one feed

- Dedicated ad-platform cards — Facebook Ads, Google Ads, Multi Ads cards optimized to bypass decline filters

- API integration — programmatically issue cards, monitor balances, automate top-ups from your backend

- White-label solutions — launch your own branded cryptocard service using LinkPay's tech stack

For an agency running 10+ active ad campaigns across Meta, Google, and TikTok, this consolidates spending visibility and reduces operational overhead significantly. The Pro plan (20 team members, 15 free cards) is the realistic entry point; Ultra (50 members, 79 cards) for larger operations.

⚖️ Who LinkPay actually suits?

Strong fit:

- Ad agencies and media buyers — dedicated Facebook / Google / Multi-Ads cards solve chronic decline problem

- Users who want no-KYC virtual cards — only email required, no passport / liveness / address verification

- Crypto holders who need quick fiat utility — instant conversion BTC/USDT → USD/EUR card balance

- Entrepreneurs wanting white-label or API access — full programmatic integration available

- OnlyFans creators or contractors — dedicated withdrawal solutions for adult-platform earnings

Not ideal:

- Pure retail crypto holders seeking only cashback — Bybit Card / Pionex Card / OKX Card are simpler with KYC overhead

- Users wanting government-insured balances — LinkPay isn't FDIC / EU deposit-guaranteed

- Holders of altcoins outside BTC/USDT — convert first via DEX/CEX before depositing

- Anyone needing crypto staking yield on the card balance — LinkPay doesn't offer card-balance APY (Pionex 5%, OKX 10% for that use case)

🔧 How to start — 5-step setup

- Sign up via my referral link — email / Gmail / Telegram login, ~30 seconds

- Verify email immediately — activates full feature suite

- Pick a plan — Lite is free if just testing; Plus/Pro/Ultra for serious spending

- Issue your first card — choose category (Daily Omni for general use, or specialized for ads), specify cardholder name, choose currency (USD/EUR)

- Deposit BTC or USDT — send to your LinkPay address, auto-converts on arrival, lands on card balance

Once card has balance, add to Apple Pay / Google Pay and you can spend anywhere Visa or Mastercard is accepted.

💎 Bottom line — sign up if...

LinkPay is the bridge crypto-card category was waiting for. Fast, no-KYC, professional, and removes the friction from Web3 lifestyle for both retail users and agencies. The 2.9% card-top fee on Ultra plan plus 2% cashback puts it on par with the better CEX cards, but without KYC overhead and with specialized ad-platform cards that solve the chronic decline problem.

Main reasons to sign up:

- No-KYC virtual Visa / Mastercard in seconds

- Apple Pay + Google Pay out of the box

- Dedicated ad-platform cards (Facebook, Google, Multi-Ads) bypass standard decline filters

- Up to 79 free cards/month on Ultra plan

- 2% cashback on Ultra, 1% on Pro

- 50% referral commission — competitive vs CEX affiliate programs

- Team Wallet for agencies — 5 / 20 / 50 team members depending on plan

- API + white label available for entrepreneurs

Main caveats:

- No-KYC ≠ unlimited — large or unusual spending may trigger automated review

- Card balance is custodied by LinkPay, no government deposit insurance

- BTC and USDT only for now (ETH and others on roadmap)

- Regulatory grey zone — verify availability for your jurisdiction before depositing serious capital

💳 Sign up to LinkPay via my referral link — Lite is free to start, first card in seconds.

⚠️ Final note: LinkPay isn't a financial advisor, neither am I. Fees, plans, available card categories and regulatory status may change. Don't keep more than monthly spending volume on the card balance. Educational content, not financial advice.

🔗 Related articles

- Bybit Card review 2026 — up to 10% cashback / 5 free subscriptions — CEX-issued KYC card with stronger cashback at higher tiers

- Crypto Cards 2026 — full comparison — LinkPay vs Bybit vs OKX vs other major options

- BloFin review 2026 — futures and copy trading — CEX alternative for crypto-margin trading

- Bitrue review 2026 — TradFi tokens + crypto — multi-asset exchange with tokenized stocks

Register via my link

Sign up to LinkPay through my referral linkFrequently asked

What is LinkPay and how is it different from a CEX-issued card?+

LinkPay is a non-custodial fintech platform that instantly converts crypto deposits (BTC, USDT) into virtual Visa or Mastercard balances issued in USD or EUR. Unlike Bybit Card, OKX Card or Pionex Card — which require KYC and are tied to a specific exchange — LinkPay needs only an email (or Gmail / Telegram login) and supports Apple Pay and Google Pay out of the box. Crypto deposits are converted at the moment they hit your LinkPay address, so the platform itself doesn't custody your trading balance long-term — only the card balance. Second structural difference: LinkPay specializes in business use cases (Facebook Ads, Google Ads, OnlyFans withdrawals, agency team-card management) which CEX cards don't address. For pure retail spending Bybit Card has better cashback at Tier 3+, but for ads payment and no-KYC virtual cards LinkPay is structurally unique.

How much does LinkPay actually cost to use?+

LinkPay has four pricing plans visible on the pricing screenshot. **Lite (Free)**: Card top fee 4.9%, Deposit fee 1%/min$0, Transaction fee 2%/min$2, 0% cashback, 0 free cards/month, 3 team members. **Plus ($59/mo)**: Card top fee 4.5%, Deposit 0.75%, Transaction 1.5%/min$1, 0% cashback, 5 free cards. **Pro ($179/mo)** Most popular: Card top fee 3.9%, Deposit free, Transaction 1%, 1% cashback, 15 free cards, 20 team members. **Ultra ($209/mo)** Best deal: Card top fee 2.9%, Deposit 0%, Transaction 1%, **2% cashback**, **79 free cards**, 50 team members, 0% processing fee. Break-even math: Plus is worth it from ~$1,300/month volume, Pro from ~$5,000/month, Ultra from ~$15,000/month if you maximize cards and cashback. For occasional retail use stick with Lite. For ads buying or agencies Pro or Ultra wins quickly.

What cards does LinkPay offer and what are they actually for?+

Four main card categories visible on the screenshots: **Facebook Ads Card** — preferred solution for paying advertising bills on Meta platforms (Facebook, Instagram), eliminates Risk Payment notifications in Facebook Ads Manager. **Google Ads Card** — most reliable payment method for Google Ads campaigns, eliminates Suspicious Payment Activity alerts. **Multi Ads Card** — specially designed for ads on Google, Facebook, Twitter, Bing, Taboola and others. **Daily Card (Omni)** — universal card for booking hotels, Airbnb, hosting on Digital Ocean or Amazon, with 3-D Secure support. All cards include 3-D Secure verification, 0% deposit fee, and 2% cashback (when on Ultra plan). Each card has its own number and can be issued/cancelled instantly from the dashboard — useful for isolating spend categories or stopping fraud quickly without affecting your main payment method.

Is LinkPay really no-KYC?+

Yes for account registration and basic card usage. Sign-up requires only email (or Gmail/Telegram login), no passport, no selfie, no proof of address. This is structurally different from CEX-issued cards (Bybit, OKX, Coinbase) which require full KYC including liveness checks and address verification. For LinkPay you get a working virtual card issued in your name (you specify First Name and Last Name on the issue dialog — no document verification against this) and you can spend immediately. **Important caveat:** transaction limits and risk-monitoring still apply. Large or unusual spending patterns can trigger automated review; very high single transactions may require additional verification. For typical retail or agency-scale ad spending (up to several thousand USD/month per card) you operate fully no-KYC. For institutional volumes (50K+/month per card) expect compliance touchpoints regardless of platform.

How does the cashback actually work?+

Cashback depends entirely on your plan. **Lite and Plus**: 0% cashback. **Pro**: 1% on eligible purchases. **Ultra**: 2% on all purchases (this is the maximum). Cashback is credited automatically per transaction in the same currency as the card balance (USD or EUR). There's no points system, no redemption process, no waiting period — it just lands in your LinkPay balance. For comparison: Bybit Card retail tier gives 2% on all stablecoin spending, Pionex Card gives 1% USDT on most categories, OKX Card gives 2% Non-VIP but only on USDG specifically. LinkPay Ultra at 2% is competitive with the better CEX cards while keeping the no-KYC structural advantage. The breakeven: if you spend $11,000/month on cards, Ultra plan ($209) pays for itself in cashback alone (2% × $11K = $220). Below that volume, Pro or Plus is more economical.

Does LinkPay support businesses and ad agencies?+

Yes, this is one of LinkPay's strongest verticals. Team Wallet feature on the dashboard allows you to issue cards for staff members, set granular spending limits per card, and track every transaction from one master dashboard. Plus plan supports 5 team members, Pro plan supports 20, Ultra plan supports 50. For media buyers running campaigns on Facebook / Google / TikTok / Twitter / Bing / Taboola, dedicated category cards solve the chronic problem of card declines on ad platforms (especially Meta, which aggressively blocks new payment methods). Each ad-platform card is whitelist-optimized for that specific destination, reducing decline rates significantly. Additionally LinkPay offers full **API integration** and **white-label** solutions — you can launch your own branded cryptocard service using LinkPay's tech stack, which is interesting for agencies wanting to offer cards to their own clients.

What about the referral program?+

LinkPay offers up to **50% commission** on fees paid by users you refer. Tracking is real-time, payouts go to your LinkPay balance. Calculator on the referral page shows realistic projection: 20 referrals × $1,000 average daily volume = approximately $504/month potential income (plus $0.20 per registration). This is more competitive than most CEX affiliate programs (which typically cap at 30-40%). The model rewards bringing active users (not just signups) — passive registrations contribute minimally, but high-volume users referred from your link generate ongoing flow. If you have an audience interested in crypto cards, ads buying, or no-KYC payment solutions, the referral economics work.

What are the real risks of using LinkPay?+

Five main risks to consider: 1) **Custodial nature of card balance** — while crypto deposits are auto-converted, the resulting USD/EUR balance is custodied by LinkPay. Standard counterparty risk applies. Don't keep more than monthly spending volume on the card. 2) **No deposit insurance** — unlike a US bank's FDIC or EU's deposit guarantee, LinkPay balances aren't government-protected. 3) **Geographic and regulatory uncertainty** — LinkPay operates in the crypto-card grey zone of multiple jurisdictions. Regulatory tightening (especially in EU under MiCA or US enforcement actions against unregistered card issuers) could affect availability without warning. 4) **Card decline risk on flagged platforms** — even with dedicated category cards, payment processors may flag transactions. Keep alternative payment methods for critical purchases. 5) **Currently limited asset support** — BTC and USDT only (ETH and other major alts on roadmap). If you primarily hold other assets, you need to convert first via DEX/CEX. For typical use cases these risks are manageable, but understand them before depositing meaningful capital.

Want a review like this for your project?

YouTube review + Telegram + an evergreen blog article — EN · ES · RU-CIS markets. Real audience, verifiable results.

Read next

📈 Kalshi Perpetuals Review 2026 — trading perps on a CFTC-regulated US exchange

🇯🇵 Japan Made Crypto a Financial Instrument — 55% Tax Falls to 20%, the ETF Path, and What It Means